Last November when we first explored the idea of investing according to principles of social responsibility (abbreviated to SRI), often also called Environmental, Social and Governance (ESG) investing, or simply Corporate Sustainability, we focussed on the available SRI/ESG mutual funds and ETFs and used them to look at recent performance of the stocks held in these funds.

Today, we'll return to the topic. A first motive is that those funds are the not final word on which companies merit inclusion. They do not necessarily include all stocks that meet Sustainability principles since the funds attempt to have a mix of holdings across many sectors and thus may neglect worthy companies. Second, there is growing evidence that investors can make money by paying attention to Sustainability. The paper The Added Value of ESG/SRI on Company and Portfolio Levels – What Can We Learn From Research? reviews the literature and finds a positive relationship between company financial performance and the adoption of Sustainable practises. In another paper, The Impact of Corporate Sustainability on Organizational Processes and Performance, Harvard Business School researchers Robert Eccles, Ioannis Ioannou and George Serafeim found that SRI/ESG adopters outperformed both in stock market and accounting terms. Moreover, "The outperformance is stronger in sectors where the customers are individual consumers instead of companies, companies compete on the basis of brands and reputations ...".

Therefore, we will focus on consumer facing companies.

Finding the consumer stocks

Using the free TMX Money stock screener, we selected the Consumer Defensive sector to extract an inital list, cutting it off at companies with $1 billion or more in market cap, to which we added hardware retailer Rona Inc and fast-food vendor Tim Hortons and from which we removed three companies (Saputo, Maple Leaf Foods and Canada Bread) that don't deal directly with consumers.

Getting the "green" info

Unfortunately, and hopefully this will change soon since the data is useful and important to a growing number of individual stock investors, it is not easy to get the data on how much or well companies have implemented Sustainable policies. Bloomberg and Thompson do compile such data and it is available to institutional investors paying the hefty fees but the individual investor is left to troll through corporate documents like the annual report, the management information circular (aka the proxy circular) or presentations freely available on the company Investor Relations website area or on Sedar (under the Search Database tab). So that's what we did and compiled the comparison table below, which we note may not be 100% accurate since some factors are often not very clearly explained - especially the degree to which to which executive compensation is tied to ESG results.

Three key Sustainability factors

The Harvard paper says three indicators explain best the combination of Sustainability adoption and financial success of consumer-facing companies:

The results - who is green who is not

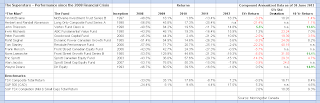

There are twelve companies in our list:

![]()

Have the more Sustainably-oriented companies attained higher profitability and stock returns?

Alas, the answer at the moment seems to be No. The company with the best trailing profitability, as seen in Return on Equity and Return on Assets, is the non-SRI/ESG Jean Coutu Group. The company with best five-year compound stock total return is Alimentation Couche Tard, also non-SRI/ESG.

It is encouraging, though we should remember that it may simply reflect the general market trend of what has been a popular sector lately, that all but two of the stocks have given off returns vastly ahead of the overall TSX index, as shown in the table by the iShares S&P/TSX Composite ETF (symbol: XIC).

All in all, the short term results are a reminder of what the researchers found. Adopting Sustainability practices is a long term strategic choice that pays off in the long term and on average. Not every high Sustainability company will do gangbusters, or even necessarily avoid major troubles. Nor will companies that ignore such practises go down the tubes or be financial laggards. The investor needs to undertake normal stock investment assessment as well.

Disclaimer: this post is my opinion only and should not be construed as investment advice. Readers should be aware that the above comparisons are not an investment recommendation. They rest on other sources, whose accuracy is not guaranteed and the article may not interpret such results correctly. Do your homework before making any decisions and consider consulting a professional advisor.

Today, we'll return to the topic. A first motive is that those funds are the not final word on which companies merit inclusion. They do not necessarily include all stocks that meet Sustainability principles since the funds attempt to have a mix of holdings across many sectors and thus may neglect worthy companies. Second, there is growing evidence that investors can make money by paying attention to Sustainability. The paper The Added Value of ESG/SRI on Company and Portfolio Levels – What Can We Learn From Research? reviews the literature and finds a positive relationship between company financial performance and the adoption of Sustainable practises. In another paper, The Impact of Corporate Sustainability on Organizational Processes and Performance, Harvard Business School researchers Robert Eccles, Ioannis Ioannou and George Serafeim found that SRI/ESG adopters outperformed both in stock market and accounting terms. Moreover, "The outperformance is stronger in sectors where the customers are individual consumers instead of companies, companies compete on the basis of brands and reputations ...".

Therefore, we will focus on consumer facing companies.

Finding the consumer stocks

Using the free TMX Money stock screener, we selected the Consumer Defensive sector to extract an inital list, cutting it off at companies with $1 billion or more in market cap, to which we added hardware retailer Rona Inc and fast-food vendor Tim Hortons and from which we removed three companies (Saputo, Maple Leaf Foods and Canada Bread) that don't deal directly with consumers.

Getting the "green" info

Unfortunately, and hopefully this will change soon since the data is useful and important to a growing number of individual stock investors, it is not easy to get the data on how much or well companies have implemented Sustainable policies. Bloomberg and Thompson do compile such data and it is available to institutional investors paying the hefty fees but the individual investor is left to troll through corporate documents like the annual report, the management information circular (aka the proxy circular) or presentations freely available on the company Investor Relations website area or on Sedar (under the Search Database tab). So that's what we did and compiled the comparison table below, which we note may not be 100% accurate since some factors are often not very clearly explained - especially the degree to which to which executive compensation is tied to ESG results.

Three key Sustainability factors

The Harvard paper says three indicators explain best the combination of Sustainability adoption and financial success of consumer-facing companies:

- Separate Board of Directors committee devoted to Sustainability - If it important enough to the company that the top level policy people are paying attention, it apparently gets done.

- Executive compensation tied to Sustainability - If the top managers' pay depends on doing it, then they tend to do it.

- Formal stakeholder engagement processes are in place - The existence of mechanisms like surveys, focus groups and audits, to engage with customers, with employees, with the communities where they operate and with suppliers reduces risk and improves adaptability of the companies.

The results - who is green who is not

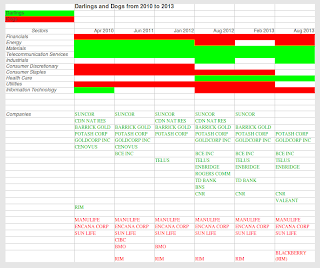

There are twelve companies in our list:

- Only three seem to have adopted none of the three key actions - Rona, Alimentation Couche-Tard and Jean Coutu.

- None has adopted every single measure either.

- All four companies that are held by the iShares Jantzi Social Index Fund (symbol: XEN) - Tim Hortons, Loblaw, Canadian Tire and Shoppers Drug Mart - have adopted at least one of the key measures. It would have been a surprise otherwise.

- Some companies do appear to be further down the path of making Sustainability an integral part of their business at every level from strategy to daily operations, notably Metro, Tim Hortons, Loblaw, Canadian Tire and Shoppers Drug Mart. Metro, Canadian Tire and Tim Hortons all regularly publish a separate report with multiple metrics on Sustainable activity and performance.

(click on image to enlarge)

Have the more Sustainably-oriented companies attained higher profitability and stock returns?

Alas, the answer at the moment seems to be No. The company with the best trailing profitability, as seen in Return on Equity and Return on Assets, is the non-SRI/ESG Jean Coutu Group. The company with best five-year compound stock total return is Alimentation Couche Tard, also non-SRI/ESG.

It is encouraging, though we should remember that it may simply reflect the general market trend of what has been a popular sector lately, that all but two of the stocks have given off returns vastly ahead of the overall TSX index, as shown in the table by the iShares S&P/TSX Composite ETF (symbol: XIC).

All in all, the short term results are a reminder of what the researchers found. Adopting Sustainability practices is a long term strategic choice that pays off in the long term and on average. Not every high Sustainability company will do gangbusters, or even necessarily avoid major troubles. Nor will companies that ignore such practises go down the tubes or be financial laggards. The investor needs to undertake normal stock investment assessment as well.

Disclaimer: this post is my opinion only and should not be construed as investment advice. Readers should be aware that the above comparisons are not an investment recommendation. They rest on other sources, whose accuracy is not guaranteed and the article may not interpret such results correctly. Do your homework before making any decisions and consider consulting a professional advisor.